Most people have tried to save money at some point. Many have made a genuine effort — the budget spreadsheet, the meal plan, the commitment to stop buying things they don’t need. And many of those efforts have faded out within a few weeks or months.

This isn’t a character failure. It’s a design failure. Most money-saving advice is designed for a version of you that has unlimited time, consistent motivation, and no competing priorities. It doesn’t account for the real conditions under which financial decisions get made: tired evenings, busy mornings, social pressure, emotional spending, and the general grind of daily life.

Sustainable money-saving habits are built differently. They’re built for the version of you that exists on a Wednesday night when you’ve had a hard day and you’re deciding between cooking and ordering delivery. That version of you isn’t going to consult a spreadsheet or summon unusual discipline. That version of you is going to default to whatever option requires the least effort.

The goal of sustainable money habits is making the cheaper option require less effort. Not more willpower. Less effort.

Why Saving Money Feels Hard

The fundamental challenge of saving money in 2026 is that the economy has become extraordinarily good at converting moments of low resistance into spending. Tired? Delivery is one tap away. Bored? Streaming is already paid for and infinite. Stressed? Retail therapy is available 24 hours a day with free returns.

The barriers to spending have been systematically dismantled. Payment is saved, delivery is fast, returns are easy, trials are free. The machinery of commerce is specifically optimized to minimize the moment between “I want this” and “I bought this.”

Against this backdrop, the advice to “just exercise more willpower” is genuinely inadequate. Willpower is a finite daily resource. You use it in difficult conversations at work, in managing stress, in maintaining any difficult habit you’ve committed to. By 9 PM most evenings, willpower reserves are low. The system wins.

The alternative isn’t more discipline. It’s designing your environment so the default choice is cheaper. That’s what all the recommendations in this guide are trying to do.

Food Habit Change — Designing the Path of Least Resistance

The question is never whether home-cooked food is cheaper than restaurant food. It is, consistently, by a wide margin. The question is whether the path to home-cooked food is short enough on any given evening that you’ll take it over ordering delivery.

Meal prep containers as infrastructure. A set of glass meal prep containers (Prep Naturals or Bayco, $28–$38) filled every Sunday changes the calculation. The question on Wednesday night isn’t “do I have the energy to cook?” — it’s “do I have the energy to assemble?” Assembly — reheating prepped grains, adding pre-cut vegetables and pre-cooked protein, pouring on a sauce — takes 10–15 minutes. Most people can do that even on a hard day.

The Sunday prep habit is the thing. The containers are the infrastructure that makes the habit work. Without containers, prepped food gets mixed together, portions get uncertain, and the fridge looks like a mess rather than a meal plan. With containers, it looks organized and appetizing and it gets eaten.

The grocery receipt habit. One of the lower-effort food habit changes: look at your grocery receipts. Actually read them. Add up the category of things that went bad before you used them. For most households, this number is significant enough — in the $20–$50 per month range — that it shifts shopping behavior without requiring any additional instruction.

Cooking more of the same things. Culinary variety is aspirational. Cooking 8–10 recipes you know well and enjoy is sustainable. The meals that don’t require looking up a recipe, buying special ingredients, or learning a new technique are the meals that actually happen on a weeknight. Build a rotation of genuinely good, genuinely simple dishes and cook those. The savings come from buying the same ingredients repeatedly (better prices, less waste) and from the time efficiency of familiar recipes.

Shopping Habit Change — The Low-Tech Approaches That Work

The purchase waiting period. Before any non-essential purchase over $30, wait 48–72 hours. Not as a rule you enforce through willpower, but as a system: items go in a cart or a list, not in your possession. When you come back after 48–72 hours, some percentage of those purchases no longer seem compelling. That percentage is money saved without any denial in the moment.

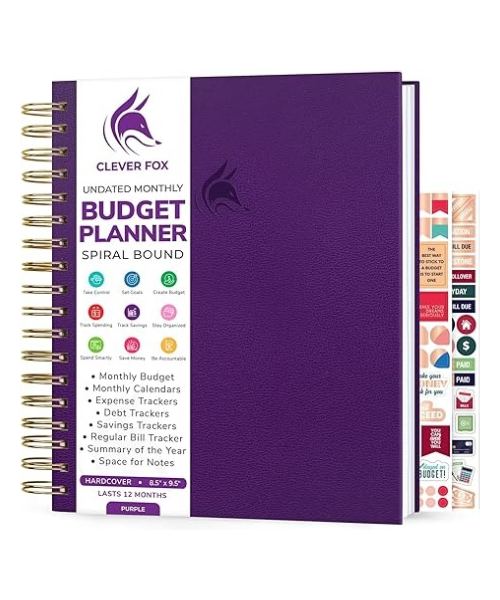

Budget planner for monthly spending allocation. The Clever Fox Budget Planner ($22–$28) or a simple two-column notebook works for this purpose. At the beginning of each month, allocate your after-necessities income across discretionary categories — food, entertainment, clothing, household, personal. Once a category is spent, it’s spent for the month.

The psychological effect of a physical budget is different from a mental one. Mental budgets are vague and flexible. Physical budgets have visible limits. When the “clothing” line is filled in and there’s $0 remaining, the question “should I buy this shirt?” has an easy, non-willpower-requiring answer.

Unsubscribing from all retail email. This is the lowest-effort shopping habit change available and it’s underused. Retail emails exist to create purchasing impulses, not to inform purchasing decisions. They’re designed to manufacture urgency through sale countdowns, limited stock warnings, and personalized recommendations. Every email that doesn’t arrive is a trigger that doesn’t fire.

Home Habit Change — Where Habits Have Compounding Effects

The coffee at home habit, designed for real mornings. A programmable drip coffee maker set up the night before and programmed to brew 15 minutes before you wake up changes the morning equation significantly. The coffee is there. It’s good. It’s warm. The coffee shop requires getting dressed, driving, waiting, and spending $5. The path of least resistance shifted.

Hamilton Beach Programmable 12-cup ($35–$40) is the practical recommendation here — nothing flashy, reliable, programmable, easy to clean. The ritual of setting it up the night before (filling the reservoir, setting the timer) takes 3 minutes. The morning benefit is disproportionate to the effort.

Reusable water bottle — the honest version. A quality insulated water bottle (Owala FreeSip at $32–$35, or Hydro Flask at $35–$40) saves money proportional to how often you currently buy beverages away from home. If you spend $2–$3 daily on bottled water, the bottle pays for itself in about 2 weeks. If you primarily drink tap water at home and rarely buy drinks out, the bottle is convenient but not a significant money-saver.

The habit that makes it work: filling it before you leave the house every morning. Same place, same time, same ritual. Once it’s a morning default, it operates without thought.

Storage boxes for pantry visibility. A disorganized pantry is an expensive pantry — things expire behind other things, ingredients get forgotten, duplicates get purchased. A single afternoon spent organizing the pantry with uniform clear storage boxes (Sterilite 6-quart at $4–$6 each, or IKEA SAMLA at $3–$8) pays dividends in reduced waste and fewer “I thought we were out of this” purchases. The investment is $20–$40 and a few hours. The ongoing benefit is permanent.

Subscription Cleanup — One Annual Task Worth Prioritizing

Subscription fees are engineered to stay beneath your attention threshold. They’re small enough individually that they don’t register as significant expenses, but they aggregate to meaningful monthly spending that most people underestimate by 40–60% when asked.

Once per year — your birthday, New Year’s, or any arbitrary date you mark on a calendar — do the audit. Bank statements, 60 days, every recurring charge on the list. For each one: have I used this consistently this year? Would I subscribe today if I were starting fresh?

The subscriptions that survive this review are earning their cost. The ones that don’t survive were quietly wasting money that could go anywhere more useful.

The emotional difficulty: some subscriptions have identity value beyond their use value. A gym membership you don’t use but keep because you intend to start going. A professional development subscription you keep because it represents who you want to be. These are valid feelings, but they’re worth being honest about. Paying $35/month for an intention rather than a service is an expensive way to feel aspirational.

Things Worth Spending On

Good cookware that makes cooking enjoyable. A single decent chef’s knife ($40–$60), a heavy-bottomed pan ($30–$50), and a large pot ($25–$40) are the equipment that makes the cooking habit sustainable. Cooking with bad equipment is a friction source that accumulates into avoidance. Cooking with good equipment is genuinely pleasant.

Fresh, quality ingredients. The version of budget cooking where you eat food you don’t enjoy is the version that fails. The version where you cook simple food with fresh, quality ingredients is the version that sticks. Buy good olive oil. Buy the protein you actually like. The savings come from cooking at home, not from eating subpar food at home.

A physical budget planner. The specific investment in a tool for managing money is worthwhile for anyone who has found digital tools don’t create the engagement needed for consistent budgeting. The physical version requires a different kind of interaction — you have to pick it up, open it, write in it — that creates stronger behavioral commitment for many people.

Products That Help Save Money

The batch cooking infrastructure. Glass keeps food looking appealing, reduces odor transfer, and lasts indefinitely. Worth the modest premium over plastic for daily use.

Replaces bottled beverage spending for people with that habit. The push-button lid is genuinely bag-safe and the dual-drink design — sip or swig — reduces daily friction compared to bottles that require unscrewing a lid.

The programmability is the key feature — it removes the morning friction of coffee making by making it the night before’s job, not the morning’s. Reliable, easy to clean, produces decent coffee from quality beans.

Monthly budget allocation, irregular expense tracking, and savings goals in one physical book. The annual and quarterly review sections are particularly useful for identifying spending drift over time.

Pantry and home organization infrastructure. Clear sides make inventory visible without opening. Stackable design maximizes cabinet space. The financial benefit is indirect but real — organized storage reduces forgotten-item waste and duplicate purchases.

Final Thoughts

The money-saving habits that work over years are almost always the boring ones. Not the dramatic gestures — selling your car, moving to a cheaper city, cutting all entertainment. The boring ones: meal prepping on Sundays, filling a water bottle before you leave the house, checking your bank statements monthly, cancelling one subscription per year that you don’t use.

These habits don’t feel transformative. They don’t make for compelling social media content. They don’t produce dramatic before-and-after financial photos. They produce slow, steady improvement that compounds quietly into real financial stability over time.

Build the easy version of each habit first. Use the simplest tool that makes it work. Don’t optimize before you’ve established the behavior. And be honest with yourself about what you’ll actually do on a Tuesday night when you’re tired — that version of you is who your habits need to work for.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}